Private capital secondaries market

Definition – The private capital secondaries market is the only way private markets investors (or LPs) are able to exit early from their investments. It also allows fund managers (or GPs) to provide additional liquidity options to their investors.

How does secondary investing work?

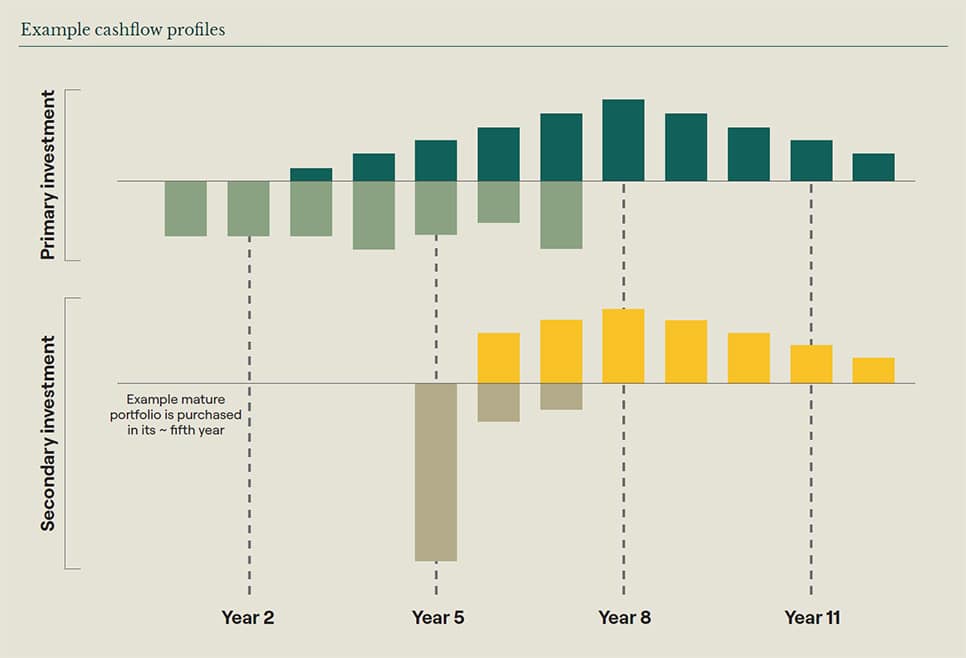

The fundamental differences between primary and secondary investing are illustrated in the example cashflow profiles below:

Primary investing

Primary investing involves committing capital to a GP’s fund without knowledge of the assets the GP will invest in. During the investment period, capital is drawn from the investor’s commitments and the GP invests in underlying assets. This means LPs experience a few years where their capital is drawn, and no capital is returned to them. Over time, as the underlying assets are sold, capital is distributed back to LPs

Secondary investing

In contrast, secondary investing involves the acquisition of mature, substantially invested portfolios, often at a discount to NAV, avoiding the ‘blind pool’ risk of the primary investment. Given the investments are more mature than those made by primary funds, these distributions can be passed back to secondary fund investors faster. Also, secondary funds are typically much more diversified than primary funds.

Evolution of the private capital secondaries market

Phase 1, development – 1990–2009

In its early stage, the secondaries market was principally the sale and purchase of limited partner interests, and later embraced interests in private assets not held in fund structures, known as direct secondaries. Market growth was incremental, driven by a small number of participants. There was little in the way of market infrastructure, with many transactions executed on a bilateral basis.

Phase 2, institutionalisation – 2010–2016

From 2010 the secondaries market began to mature, with a growing universe of buyers and sellers. In line with this, transaction volume grew, as a number of GPs joined Coller in raising dedicated secondaries funds.

Phase 3, expansion – 2017–present

Since 2017, the secondaries market has experienced near continuous rapid growth, as private markets have grown in scale and scope. Transactions are occurring on a wider number of strategies within private markets and are evolving to meet all types of liquidity needs.

As the market has expanded, so has the buyside landscape, with dedicated specialist funds being raised as institutional investors seek specific risk/reward profiles for secondaries. Given the stage of the secondaries market’s evolution, and its potential for growth, we believe that annual volume could be in excess of $500bn by 2030.